Build Trust in Every Payout Flow with iPiD

Automate Disbursement Accuracy

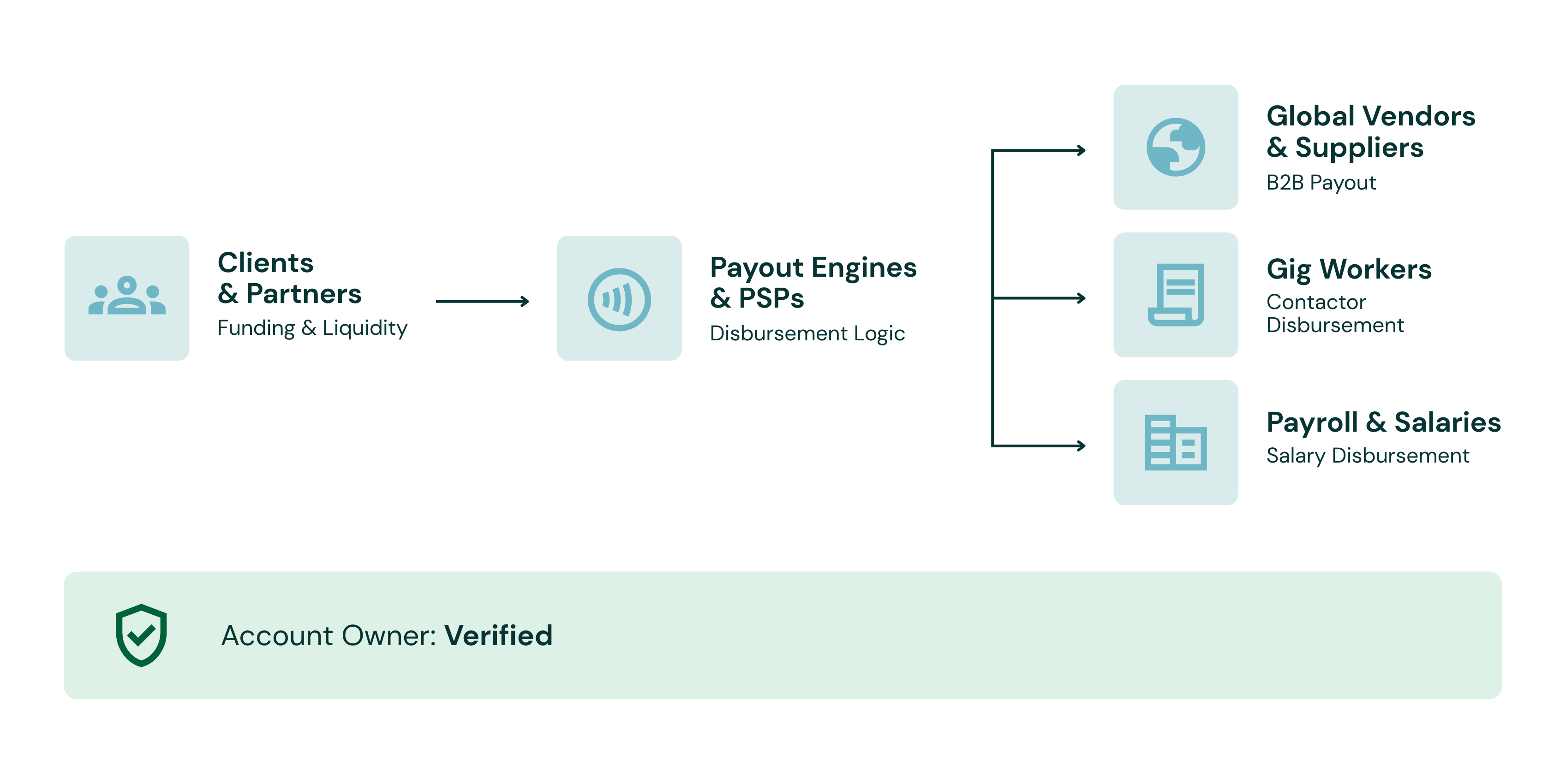

Instantly match beneficiary names with account ownership to ensure payouts reach the intended recipient every time, regardless of the destination bank.

Secure Your Payout Ecosystem

Protect your platform from impersonation scams by verifying the ultimate beneficiary identity before the transaction is authorized.

Maximize Operational Efficiency

Eliminate manual back-office churn and expensive investigation costs by catching account errors before they enter the global payment network.

.png)