From November 2026, SWIFT cross-border payment messages will need to carry structured or hybrid postal addresses. Fully unstructured postal addresses will be decommissioned, and payment messages that do not follow the required format may be rejected or delayed.

At first glance, this may look like a formatting update. In practice, it is a data-readiness challenge tied to SWIFT ISO 20022 structured addresses.

Payment messages can only be structured if the underlying address data is complete, accurate, and usable before the payment is sent. For many organizations, that data still sits across legacy systems, saved beneficiary records, corporate payment files, customer databases, and front-end payment flows in free-text form.

The result is a simple but important question: are your systems ready to turn messy address data into structured payment data before the deadline?

What is Changing in November 2026?

SWIFT is removing fully unstructured postal addresses from CBPR+ payment messages. After the deadline, payment messages will need to include either fully structured or hybrid postal addresses.

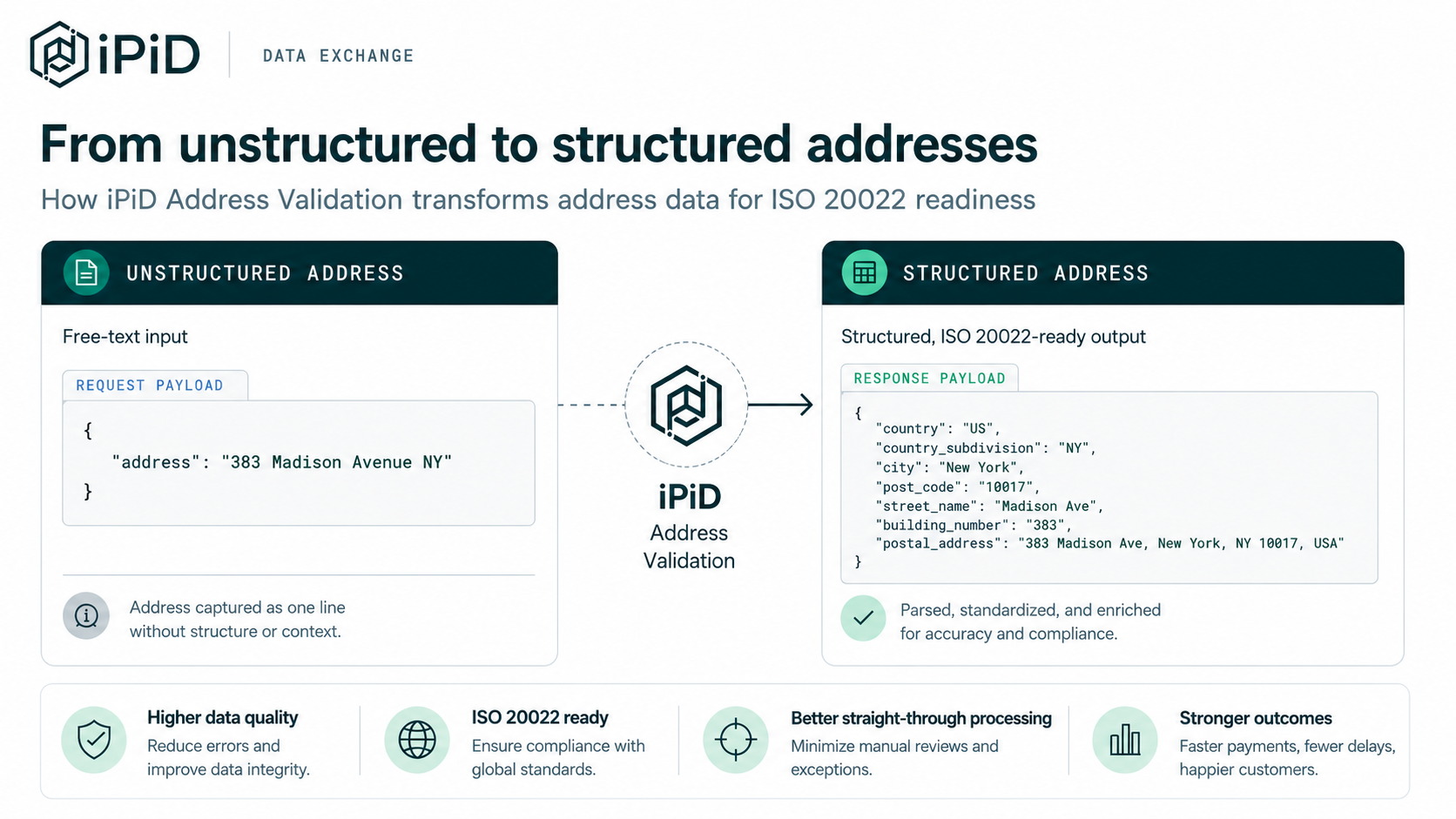

A fully structured address separates address components into dedicated ISO 20022 fields, such as street name, building number, town name, postcode, and country. A hybrid address still allows some address information to remain in an address line, but town and country must be provided in designated structured fields. This distinction is central to the new ISO 20022 address format.

At minimum, town and country information must be provided in the correct fields. This applies across a broad set of payment types, including corporate, trade, FX, securities, and funds.

For banks, PSPs, and ERP or treasury platforms, the SWIFT 2026 address requirements are not just about the final message. They also affect how address data is collected, stored, validated, and transformed upstream.

Why This Matters: Payment Rejects are Only the Visible Risk

The most obvious risk is that payment messages may be rejected or delayed if address data does not meet the required format. That alone creates urgency, especially for institutions and providers processing high volumes of cross-border payments.

But rejection is only the visible part of the problem.

Behind every failed or delayed payment is a chain of operational work: investigation, manual repair, customer follow-up, file correction, resubmission, and possible escalation. For banks and PSPs, this can increase operational overhead and slow down payment processing. For corporates, it can affect supplier payments, treasury operations, and customer experience.

The deeper issue is that many organizations do not only need to update how they send payment messages. They need to understand whether their upstream address data is good enough to support the new standard and broader ISO 20022 compliance 2026 readiness.

Who is Affected?

The deadline affects multiple players across the payment chain, but the challenge appears in different places.

For banks and financial institutions, the work is likely to touch payment channels, corporate banking portals, host-to-host files, saved beneficiary records, and payment operations. SWIFT notes that financial institutions need to structure existing customer address data, ensure channel applications can capture and validate structured address information, and engage customers early on what data they need to provide.

For PSPs and cross-border payment platforms, the risk sits in beneficiary onboarding, payout flows, partner bank requirements, and cross-border payment operations. If address data is incomplete or unstructured, payouts may be delayed, rejected, or pushed into manual handling. This makes cross-border payment address validation increasingly important before payment submission.

For ERP and treasury management providers, the issue often starts even earlier. Corporate payment data may originate from vendor master records, supplier onboarding flows, or treasury payment files. SWIFT notes that corporates must source creditor address information through their own channels, store it in ERP or treasury applications, and provide it to the bank at payment initiation.

The deadline is the same for everyone. The operational burden depends on where address data enters the payment flow.

Why This is Not Just a Technical Mapping Exercise

It may be tempting to view the SWIFT 2026 update as a field-mapping project: take address data from one system, place it into the correct ISO 20022 fields, and move on.

In reality, mapping only works if the source data is usable.

Many organizations still store postal addresses as one free-text block. Address formats vary by country. Records may be incomplete, outdated, duplicated, or inconsistent. Some corporate payment files may not pass address components in the required fields. Some front-end payment journeys may need to collect more structured data.

This is where the real work starts: identifying where unstructured address data exists today, which payment flows are most exposed, and whether teams can parse, enrich, correct, and validate addresses globally before the deadline.

This is where SWIFT payment address validation becomes more than a formatting step. The hard part is not simply creating an ISO 20022 message. The hard part is turning messy, partial, and inconsistent address data into something that can be trusted before the payment is sent.

Where iPiD Address Validation Fits

iPiD Address Validation helps bridge the gap between unstructured source data and structured payment requirements, especially as SWIFT unstructured address removal approaches.

Instead of treating poor address data as a post-payment repair issue, iPiD Address Validation allows teams to check, structure, and improve address data before the payment is sent.

iPiD Address Validation helps turn free-text addresses into ISO 20022-ready structured payloads. It can be used via API, in bulk, or as part of a broader iPiD setup. For banks, PSPs, and ERP or treasury platforms preparing for CBPR+ structured address requirements, this helps improve address data quality ahead of the November 2026 deadline.

Together with Know Your Payee (KYP) verification, iPiD Address Validation can also support a more complete “verify before you pay” workflow. Payee verification helps confirm that the name and account details match. iPiD Address Validation adds another layer by checking whether address data is complete, structured, and ready for compliant payment messages.

The November 2026 deadline may feel like a standards change, but readiness depends on the quality of address data across the payment chain. Organizations should start by understanding where unstructured addresses exist today, which payment flows are most exposed, and how they will convert messy address data into structured or hybrid formats before payments are submitted.

If your team is reviewing SWIFT 2026 readiness, we can help assess where iPiD Address Validation fits into your broader payment validation strategy.

- SWIFT - ISO 20022 milestone for November 2026: Unstructured addresses to be removed (March 2026)

- SWIFT – ISO20022 Standards – Removal of unstructured address

- SWIFT - Address structuring requirements factsheet (October 2025)